Richard Drury/DigitalVision via Getty Images

Global-e Online (NASDAQ:GLBE) just delivered excellent results considering that many other ecommerce companies including the company’s partner and investor Shopify (NYSE:SHOP) have produced rather lackluster results lately due to fading pandemic benefits. Despite the excellent results the company has been putting up, the stock of Global-e Online, like most e-commerce companies, has collapsed since the beginning of 2022.

Likewise, the valuation of the company has taken a dive, even though the company’s underlying fundamentals remain strong amid Q4 2021 results showing the company beating analyst estimates on both the top and bottom line with excellent growth expectations moving forward. The company has an excellent balance sheet with no long-term debt and positive cash flows. In addition, the company has an elite net dollar retention rate (NDR) and a very strong gross retention rate (GDR) showing Global-e Online’s domination of the greenfield niche of Direct to Consumer (D2C) Cross-Border Ecommerce. This is a segment of ecommerce that is directly fueled by millennial spend and is growing significantly faster than the overall e-commerce market.

Even though the company is still young, I don’t consider it all that speculative considering the overall trends favoring Direct to Consumer (D2C) Cross-Border Ecommerce, in addition to the quality of customers this company is already attracting. Of the many small growth companies that I have looked at, I believe Global-e is among the best to navigate a rising interest rate environment.

As I write this, Global-e has a PS ratio of 24.3. If this was a bull market, it is likely this stock would be valued far higher considering the current strong results and the fact that Global-e has barely tapped its overall opportunity. When considering the steady growth that the company is producing and the excellent forward guidance in a market where many of its peer-commerce companies are not performing quite as well, Global-e Online deserves a premium valuation and is currently a buy for growth investors.

Global-e PS Ratio (Gurufocus)

Global-e Online Q4 2021 Earnings

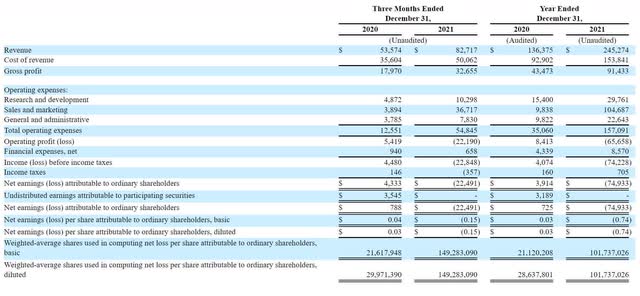

Global-e online selected data (Global-e Online Form 6-K)

The first thing I like looking at with online market places is Gross Merchandise Value (GMV) because generally this metric is the best at determining the overall health of an ecommerce marketplace. What we want to see here is a rapidly expanding GMV because the faster the GMV growth is, the healthier the overall revenue growth is. Global-e Online produced $505 million GMV in the fourth quarter of 2021, which is 66% year-over-year growth, which is a number outpacing total revenue growth. For the full year 2021, Global-e posted 87% growth in GMV. These results showed very healthy growth in GMV on both a quarterly and full year basis, despite the fact that the impact that the pandemic had in increasing ecommerce activity worldwide is tapering off. One other pandemic-related factor that Global-e Online seems to be successfully overcoming is worldwide broken supply chains issues, which is amazing since there has recently been a lot of stress on retailers that lack large logistic supply chains.

It is also worthwhile mentioning, that given our scale and the strategic relationships we have with a variety of logistics service providers, coupled with the fact that merchants tend to prioritize direct to consumer over other channels, to date we have not witnessed any meaningful impact from supply chain challenges or merchant inventory shortages.

Source: CEO Amir Schlachet – Global-e Online Q4 2021 Earnings Call

The second metric that I really like about Global-e Online is that it has a very strong Net Dollar Retention Rate (NDR) and Gross Dollar Retention Rate (GDR).

In general, an NDR above 120% is very good, an NDR above 130% is excellent and an NDR above 140% is considered elite. Usually, companies that maintain a high NDR ratio above 120% will over time have their stock go up over the long term. Global-e Online logged an annual NDR rate of 152% in 2021. Global-e Online’s NDR number is excellent and tells us that its products are really gaining traction with its clients.

As for the GDR rate, the max number is 100%, which means zero churn. A GDR rate above 95% is considered very good. Global-e Online came in with a GDR above 98%, which is excellent customer retention.

Next thing to look at is revenue growth. Global-e’s fourth quarter 2021 revenue was $82.7 million, an increase of 54% year over year. Service fees revenue was $35.5 million, up 73% year-over-year and fulfillment services revenue wound up being $47.2 million, up 43% year-over-year. Service revenues accounted for 43% of total revenues and fulfillment revenues accounted for 57% of revenues.

The CFO indicated in the earnings call that the higher growth rate in service fee revenues compared to fulfillment services revenues was driven by continued growth in Global-e’s multi-local approach which had the effect of changing the mix of merchant volumes on the platform. Last quarter, Global-e management indicated that fulfillment services could be affected if customers continued to move to the multi-local approach and that prediction came to pass. Global-e management, however, did indicate in this Q4 earnings call that moving forward, that although the multi-local product is expected to continue to expand, the same mix effect is not expected in future quarters.

Just as a reminder, the multi-local approach is a relatively new feature where a company can make deployments in multiple countries around the world and transact locally with customers. In the multi-local model Global-e Online usually does not provide fulfillment services as the model largely uses local shipping. This is opposed to the cross-border model where a merchant simply ships from a single territory into multiple countries and uses Global-e Online’s fulfillment services.

Global-e Online P&L (Global-e Online 6-K)

Similar to last quarter, gross profit grew far faster than revenue growth. Global-e Q4 gross profit was $32.7 million, up 82% year-over-year. Gross margins came in at 39.5% versus 33.5% in Q4 2020. The rise in gross margins was mostly due to the higher share of service fees revenue over fulfillment revenue.

Increasing gross profits and increasing gross margins in a young company are very desirable because it means that the company has more money available to invest in expanding growth initiatives, which should result in more potential for future growth.

Next up is operating expenses. Total GAAP operating Expenses were $54.84 million. GAAP Total Operating Loss was $22.19 million. These numbers can be hard to compare year over year because of the Shopify warrants-related amortization expense. These Shopify warrants come from the Global-e pre-IPO deal where Shopify established a stake in Global-e Online.

Global-e Online’s R&D operational expenses should continue to scale up, with the investment going into initiatives such as the Shopify native integrations with Global-e, the build out of the Emerging Brands division, the addition of more localization capabilities on the platform, the growing of a presence in the APAC region and more. Global-e Online’s fourth quarter R&D expenses, excluding stock-based compensation (SBC) was $8.4 million or 10.2% of revenue, versus $4.6 million or 8.7% in the same period last year. Total R&D spend with SBC in Q4 was $10.3 million.

Sales and marketing expense, excluding the amortization expenses related to the Shopify warrants and SBC came in at $6.7 million or 8.1% of revenue versus $3.6 million or 6.8% of revenue in the same period last year. Shopify warrants related amortization expense was $29.4 million. Adding the warrant expenses and SBC to the marketing expenses for the quarter gives a total of $36.7 million for S&M expense.

General and administrative expense, excluding SBC and the one-off Flow Technologies transaction-related expenses was $5.8 million or 7% of revenue versus $2.6 million or 4.8% of revenue in the same period last year. The rise in expenses is mostly due to the additional expenses that come with being a public company. Total G&A spend in Q4 came in at $7.8 million.

Global-e Online recorded a Q4 2021 GAAP net loss of $22.49 million versus a net income of $4.3 million in Q4 2020. The Shopify warrants accounted for the GAAP loss. Non-GAAP net income, excluding the Shopify warrant amortization expense was $6.9 million. Global-e Q4 GAAP EPS came in at -$0.15 beating Wall Street analyst consensus by $0.01.

EBITDA is usually stressed by the management of younger companies as a better metric to follow over net income because the early life stages of a company will often include a lot of financing and capital expenditures, which often makes it hard to compare quarter-over-quarter and year-over-year operational profitability and efficiency. So, let’s look at Global-e Online’s EBITDA numbers.

Global-e reconciliation to Adj EBITDA (Global-e Online Earnings Release)

Global-e Online’s Q4 2021 adjusted EBITDA was $11.8 million compared to $7.2 million in Q4 2020, showing that year-over-year, the core operations of the company are becoming more profitable.

Global-e Online Balance Sheet

Global-e Online Balance sheet (Seeking Alpha)

Global-e Online ended both the quarter and the year with $509 million in cash and cash equivalents, including short-term deposits and marketable securities prior to the closing of the Flow transaction.

Global-e Online had no long-term debt at the end of 2021 and is in excellent shape to pay all short-term liabilities with a quick ratio of 4.38.

Global-e Online operating cash flow in Q4 came in at $24 million compared to an operating cash flow of $33 million a year ago. Free Cash Flow was approximately $22 million in Q4 2021.

Global-e Online Guidance

Global-e Guidance (Global-e Online Earnings Release)

Global-e Online is projecting Q1 2022 GMV to be in the range of $446 million to $456 million, with the midpoint of the range showing growth of 69% versus Q2 of 2021. Revenues in the first quarter of 2022 are projected to be in the range of $74.5 million to $76.5 million, with the midpoint of the range showing growth of 64% versus Q1 of 2021. Global-e Online expects an adjusted EBITDA profit in the range of $0.7 million to $1.7 million in Q1 2022.

Global-e Online projects full year 2022 GMV to be in the range of $2.45 billion to $2.5 billion, with the midpoint of the range showing close to 70% annual growth. Full year revenues are expected to be in the range of $411 million to $421 million, with the midpoint of the range showing growth of 70%. Adjusted EBITDA profit is expected to be in the range of $38 million to $42 million. The company indicated on the earnings call that the FY2022 EBITDA will be negatively impacted by the acquisition of Flow Commerce.

Recently, Marketwatch performed an ecommerce stock screener that ranked companies based upon a two-year estimated sales CAGR and Global-e Online came in second with a two-year estimated sales CAGR of 53%. This was over stocks like Sea Limited (NYSE: SE), Jumia Technologies (NYSE: JMIA) and even Shopify, which came in with a two-year estimated sales CAGR of 34%

Global-e Online’s Emerging Brand Division

In my first article on Global-e Online that was posted last November, I mentioned that there was emerging confusion around the Global-e and Shopify partnership because Shopify had announced an initiative right after the partnership was formed that made it look like Shopify was competing with Global-e. This Shopify initiative is called Shopify Markets. The Global-e Online CEO was asked on the Q3 earnings call about Shopify Markets and he essentially said that Shopify Markets was simply a complementary solution to Global-e’s partnership because Shopify Markets was designed more for smaller SMB clients and Global-e Online’s partnership offering was geared more toward larger enterprise clients. Well, it is obvious now that Global-e likely thought not having a SMB solution was a hole in their portfolio because the company purchased Flow Commerce shortly thereafter to fill that hole.

Flow Commerce is an API-based technology that is built specifically for the needs of SMB companies or what Global-e calls likes to call emerging brands. Also, within the news release announcing the acquisition, Global-e specifically mentioned that the technology from the Flow Commerce acquisition will be used in its existing Shopify relationship.

The acquisition is expected to allow Global-e to expand the scope of its exclusive relationship with Shopify to offer certain cross-border services to a broader set of merchants on the platform in addition to its current end-to-end 3rd-party solution catering to established brands.

Source: Global-e Online news release

The acquisition was also mentioned on the Q4 earnings call by CEO Amir Schlachet where he talked about Global-e establishing an Emerging Brands division, of which Flow Commerce’s technology will be the centerpiece. This new division will be charged with establishing new sales channels for Flow Commerce’s technology and the first agreement that was signed was with Shopify. One other interesting thing that the CEO mentioned about the acquisition is that the new Emerging Brand division will be able to offer solutions to clients in white label form. I didn’t know what white label meant, so I looked it up and it essentially means when a product that is produced by one company gets rebranded and marketed for sale by another company.

Reading between the lines, I think that means that if I am some smaller brand in the USA, through Global-e’s Emerging Brands division, I could get another company in let’s say England to manufacture a “white label” product branded under my name to be sold in England. Also, this initiative is occurring in an era in which a person can start a YouTube, Tik-Tok or Instagram channel and possibly make over a million dollars a year. A majority of money on social media channels is made through advertising but many social media brand names have discovered that they can make lots of money selling branded merchandise too. I imagine a US-based social media star could probably use Global-e’s “white label” service to have branded products manufactured in foreign countries under their branded name distributed in foreign markets like Europe, for instance. So, yes, the Emerging Brands division might gain business from a SMB company with 100 employees but it also might gain business from a sole social media influencer with a YouTube channel too. I am assuming that is how it will work. In my opinion, it is a great idea to not only chase business from Enterprises but to gain smaller clients too.

Global-e Online New Clients

This quarter, in both the earnings release and in the earnings call, management identified several brands that are new to the Global-e Online platform and four of them were gained from the Shopify partnership. The brands mentioned are:

- From the LVMH group, Fenty Beauty and Fenty Skin, which are Rihanna’s cosmetics brands, as Rihanna’s full name is Robyn Rihanna Fenty.

- Yeezy-GAP, which is a collaboration between fashion brand Gap (NYSE: GPS) and Ye (formerly Kanye West).

- NVGTN (pronounced Navigation), which is a fast-growing sports clothing brand run by fitness influencer Ashleigh Schneggenburger and her husband, Brett Schneggenburger.

- FIGS, a healthcare apparel and lifestyle brand

Global-e Online Analyst Price Targets

Global-e analyst ratings (Yahoo Finance)

The above is based on 9 Wall Street analysts offering 12-month price targets for Global-e Online in the last 3 months. The average price target is $70.78 with a high forecast of $82.00 and a low forecast of $55.00. The average price target represents a 78% increase from the last price of $39.69.

Risks

Even though supply chain disruptions have not affected the company very much so far, the potential is always there that Global-e Online could eventually suffer from logistics problems. Currently, that is the greatest risk that I see for the company.

Conclusion

Global-e Online is one of the fastest growing ecommerce companies in the world today, while also putting up some of the best earnings results over the course of 2021. Global-e also has a very powerful partnership with Shopify that should only help them gain market share into the increasingly valuable niche of Direct-to-Consumer Cross-Border Ecommerce. Global-e Online is a buy for high growth investors.