I’m currently in escrow and have removed all contingencies other than the HOA contingency. After some delay, I recently received the HOA’s 2020 Financials (Audited) and 2021 Balance Sheet, but I’m having trouble assessing the HOA’s financial health. Specifically, the two main concerns that stick out to me:

-

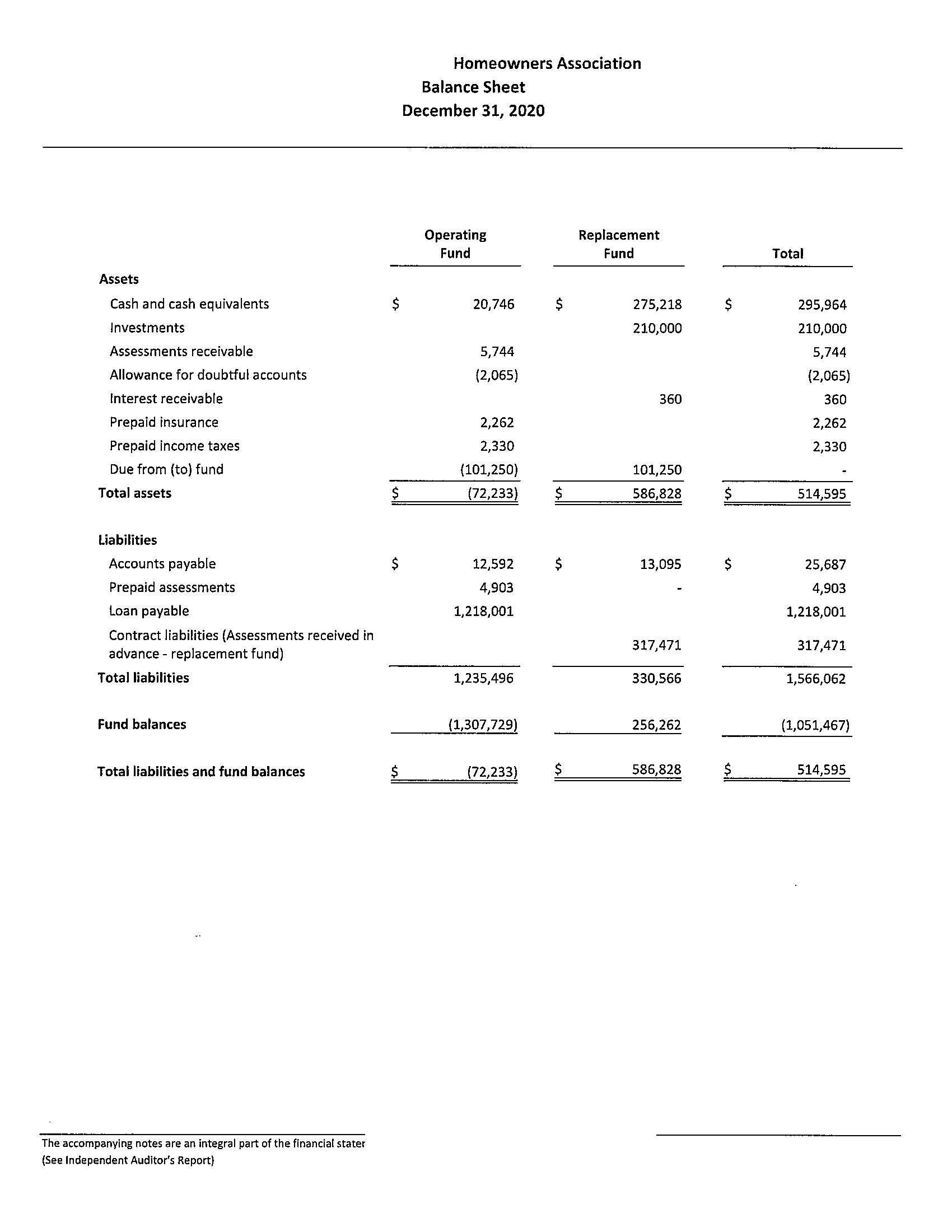

Operating Fund Deficit: The HOA covers 134 units and the HOA fees/assessments are low $300s/month which presumably means they collect ~$500k/year. But as noted in the 2020 audit notes, operating expenses exceed operating revenue. To my untrained eye, they appear to have a decent reserve/replacement fund per the 2021 balance sheet, but funding of the reserve fund appears to have dropped in 2021. This is concerning particularly due to the next concern.

-

HOA Loan: The HOA took out a $1.2 million loan in 2014 (roof) and appears to have (intentionally?) scheduled principal payments to only start in 2021. The payment schedule reflects approximately $60k-$70k/yr towards the principal from 2021-2025, and then reflects the balance of ~$870k is due “thereafter” (The loan matures in 2029).

The Twist: A few days after accepting my offer, the seller’s agent disclosed that seller is going through bankruptcy. The title report shows he filed Ch. 13 in 2016. I was annoyed but figured, as long as the court approves the sale of the home and the title report comes back otherwise clear, “Okay…Fine.” Fast forward a few weeks, as I’m reviewing the HOA documents, I see that the HOA President is…..the Seller.

So, needless to say, I have red flags going off everywhere in my head. But as a first-time homebuyer without an accounting background, this has been a bit overwhelming. At the advice of a friend, I’ve requested the HOA’s 2022 budget along with the most recent reserve study. But in the meantime, I’d be tremendously grateful if someone here would be able to provide some feedback/direction.

I’m not even sure what the right questions to ask are, but for the sake of a starting point to solicit some advice, I’ll list some here:

-

How common is it for HOAs to have insufficient reserve funds where they have to take out a loan? In this case, was an HOA loan of this size and duration reasonable ($1.2mil & 15 years)?

-

Is it typical for loan repayment schedules to be written such that they are only making interest payments for the first 7 years, until 2020?

-

What happens “thereafter,” between 2026 and 2029 when ~$870k of the balance remains? As a buyer now, will I essentially be paying more than my “fair share” for the roof?

-

CC&Rs state the HOA can increase assessments up to 20% without a vote. Is it almost certain that HOA dues will be going up beyond inflation? Will that even be enough, or is it likely that the HOA will have to issue a special assessment?

-

If you had to roughly estimate the fiscal health and management of the HOA on a scale of 1-10, what would you give it? And given this, would you back out of the deal or work with the seller to try and negotiate additional credits?

-

Any other considerations regarding the seller’s bankruptcy that I’m not thinking about? Is it atypical for bankruptcy to be pending for so long (since 2016)? It seems lengthy.

Again, thanks to the community so much for whatever knowledge you can share. As a first time homebuyer, I just want to ensure that I’m buying into a property and community that isn’t sinking or, at least, that any extreme liabilities are factored into my purchase price.